BU's emeritus Professor Nigel Jump writes the next in his series of blogs on the Dorset economy.

| RGDP (%ch Q1 2024 | +0.7 | CPIH (%ch on yr to May) | +2.8 |

| ... production (%Q/Q) | +0.6 | Unemployment (% rate Feb-Apr) | 4.4 |

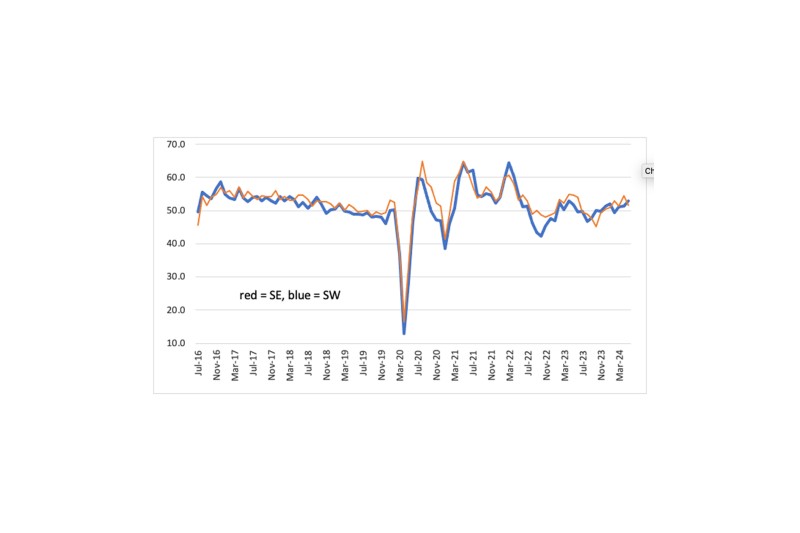

| ...services | +0.8 | SW activity PMI (May) | 51.6 |

| ...construction | -0.6 | SE activity PMI (May) | 52.9 |

RGDP = Real Gross Domestic Product

CPIH = Consumer Price Including Housing

PMI = Purchasing Managers' Index-Survey of Regional Activity

Sources ONS and SPGlobal

Output remains mixed and volatile: with services and production doing better and construction worse (see table above). April and May seem to have been rather flat but the regional PMI activity surveys have pointed to a small improvement (see chart below). The unemployment rate is edging higher and inflation rates are easing further: the headline CPI being back to the 2% in target for the year to May.

After the Election: Economics & Politics

Economics is the study of choice. With access to resources constrained, individuals/households, businesses/corporates and governments/states must decide how and where to allocate scarce resources in a way that maximises value – however measured (incomes, profits, well-being etc). Through the predominant market mechanism, economics does this by reference to absolute and relative prices - and how they influence demand and supply. Such models require trust and a fair balance of power to be reflected in trade balances, public debts and other absolute and relative monetary and real variables. It is the establishment of market power and consumption and investment incentives that links economics to politics (also about choice). Elections are our way of selecting relative priorities for state intervention in the price mechanism of economic choice. Election 2024 has resulted in a political choice for a Labour rather than a Conservative government. Whatever drove that choice, economic actors now need be prepared to react to the new “change” priorities.

The recent inflationary surge and output stagnation, around the world, reflected a range of supply side issues.

First, after policy responses to the Covid Pandemic, money supply ballooned whilst goods and services faced constrictions. Many industries are now recovering, but there are still barriers to trade in some sectors, partly reflecting the geo-politics (Ukraine, Israel, Taiwan et al) and the fragmentation of previous globalisation.

Second, regarding the balance between demand and supply for future growth, it is the supply side that needs most attention. There is a widespread need for supply side measures, (such as investment in infrastructure, capacity and skills), to build resilience, boost productivity and generate growth. “Supply creates its own demand” said Jeane Baptiste Say. “Build it and they will come” said the Field of Dreams.

The UK economy, and the local economy within it, showcases these factors. Historically, the shift in policy emphasis from demand to supply side in the 1970s and 1980s shows us examples on what we probably need right now. Trade is a vital part of this. Through negotiation, the new Labour government says it will improve the UK’s trading arrangements with Europe. But, it will not concede free movement of labour/migration or consider rejoining the EU single market or customs union. Whatever is changed, therefore, will be fragmentary: ‘nice to haves’ but not comprehensive.

During the election campaign, steps that were suggested included:

- a “Swiss-style” cutting red tape deal, accepting EU law and the jurisdiction of the European court of justice.

- Regulatory and unilateral alignment on industrial goods, such as chemicals.

- Reducing the frequency of checks by joining the Pan-Euro-Mediterranean convention. (This is a customs union agreement between the EU and 20 countries, including several in the Middle East and the Balkans.)

- A “cultural touring agreement” to make it easier for bands and orchestras to tour the continent.

- A “veterinary agreement” that could help UK food and plant exports.

- A broader “youth mobility scheme” letting 18 to 30-year-olds from the UK and EU live and work abroad. Unlikely (given migration pressures), but such a deal, or other plans to improve professional mobility, would be beneficial for local business. For example, labour market flexibility might be helped by restored ‘mutual recognition’ of professional qualifications, allowing EU and UK professionals, such as engineers, architects and accountants, to use their credentials across Europe once more.

- Cooperation on carbon taxes could also reduce paperwork and transformation frictions going forward towards net zero emissions.

Such sorts of changes may be worthwhile, but they will take time to construct.

We have an economy that is cool but slightly warming. Asset values and real incomes are driving consumption, AI is driving new jobs and activities, and both will drive the economic and social value of work. It is the supply side where sustained and sustainable productivity gains will come and where policy might intervene. Chancellor Reeves needs to be aware, however, of any unforeseen consequences of her policies on incentives for growth. The Labour Treasury should assess fully the disruptive but potentially positive scope for the next phase of UK regional development (over the rest of the 2020s).